Most people who read this column on a regular basis know I am not a big fan of reading too much into potential short-term Fed actions or other macroeconomic prognostications of the day. More often than not they are just transient noise. You do have to pay attention to the data behind those prognostications as sometimes you can see trends that could impact your investment thesis in the longer term.

One such current debate is how much longer the Fed will keep interest rates low, with one in the Fed (our own Minneapolis Fed President Kocherlakota) arguing we should continue the bond buying stimulus program as inflation is still too low.

However, are we investors focusing on the wrong longer term trend? It seems, at least to me, that there is only so much left the Fed can do. For me at least, it appears what we should be focusing on now is now what the Fed will do next but rather what will change the trajectory of money velocity in the longer term. Looking at the classic equation MV=PQ, where M is the money supply, V is velocity, P is the price level and Q is output, all seem to be doing OK except for velocity. Therefore I feel we will not reach full growth potential and acceptable levels of inflation until velocity changes. Consider the following charts:

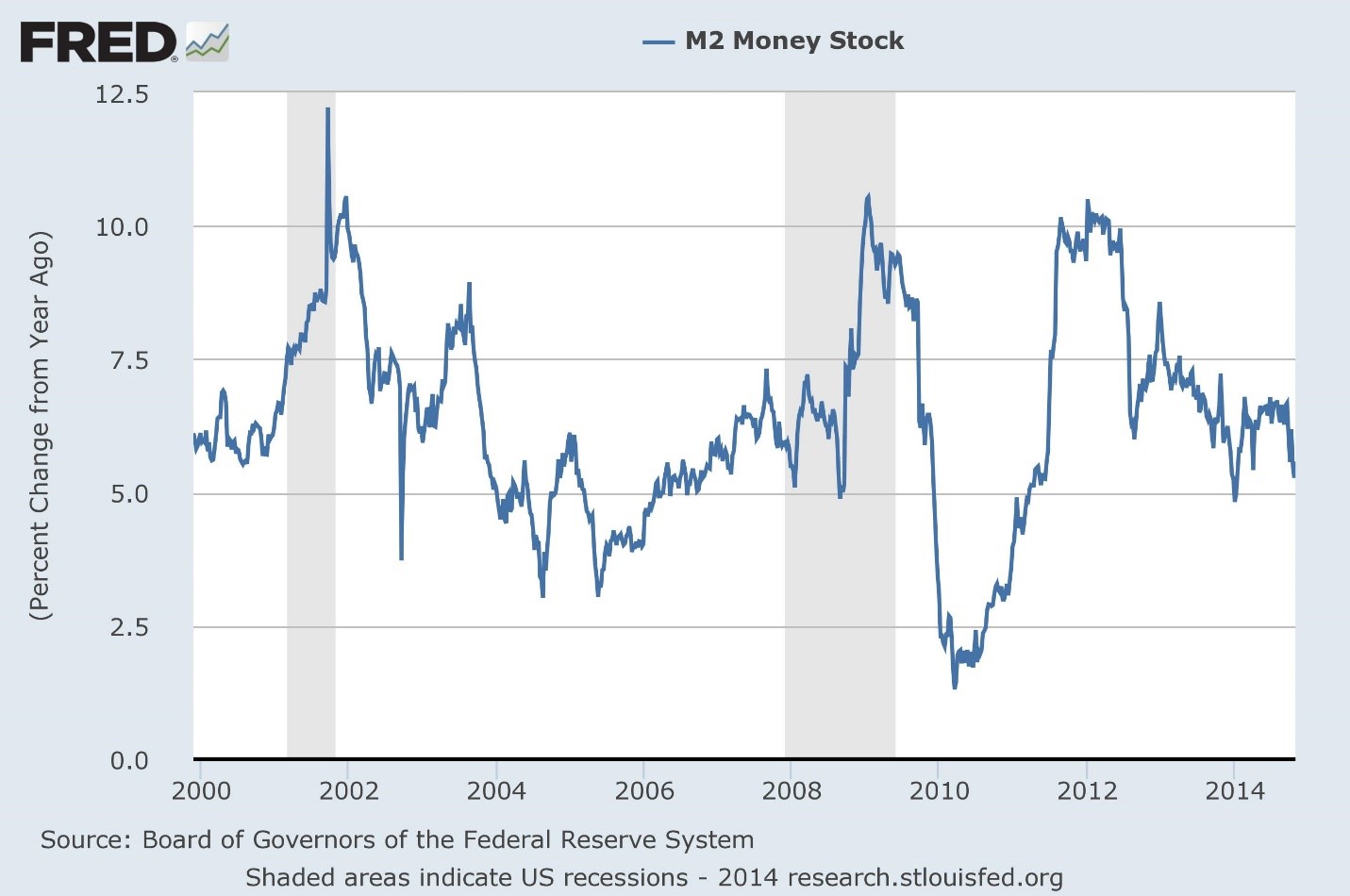

The amount of money growth in the system is within normal ranges, and was relatively elevated in the not-so-distant past.

(click on image to enlarge)

Additionally, productivity (output) seems to be holding in OK.

Source: Bureau of Labor Statistics

Inflation, as measured in CPI, likely isn’t optimal in the Fed’s view, but it doesn’t appear deflationary either and is still muddling along.

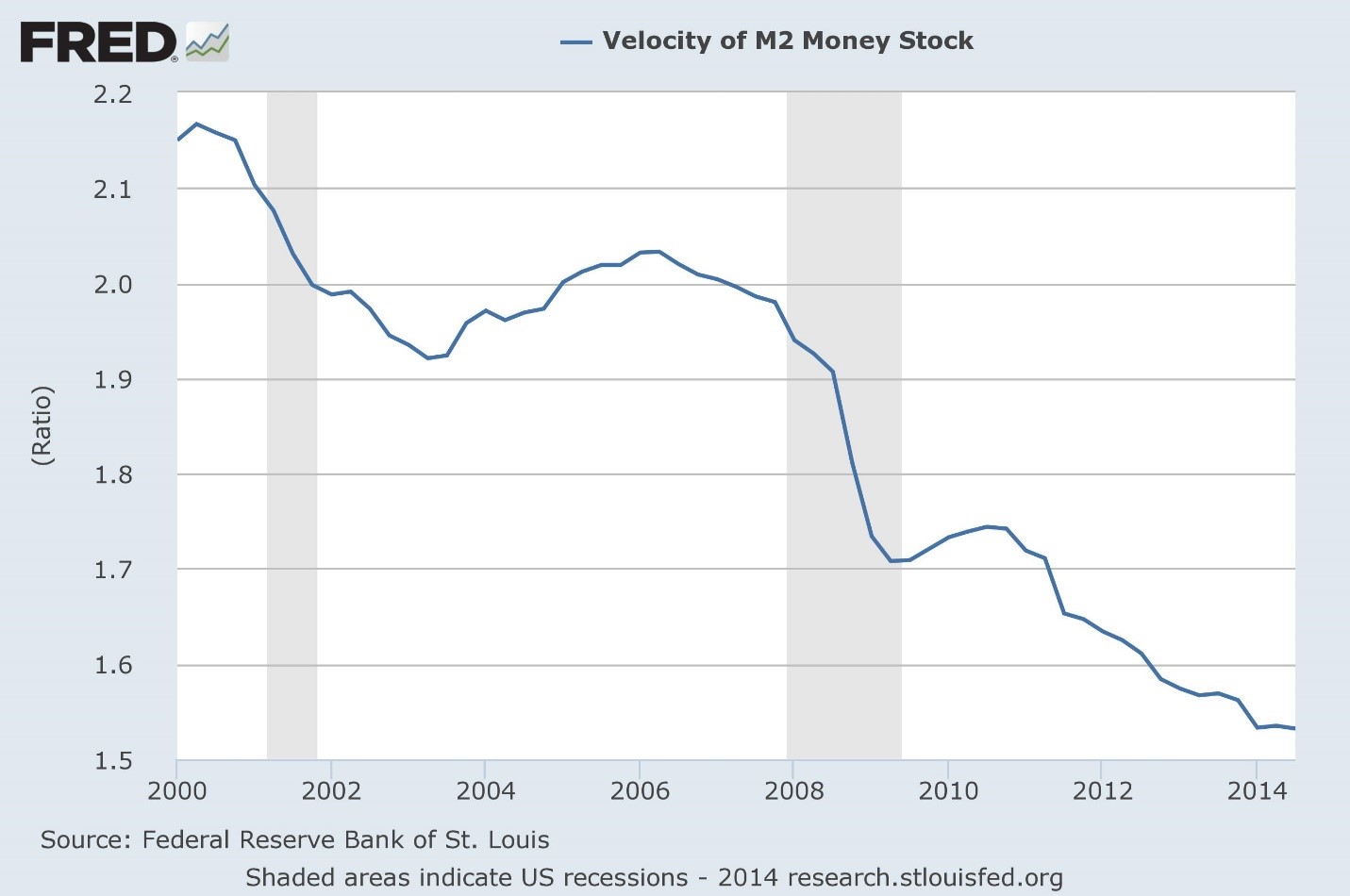

Money velocity is a different story however.

Therefore despite all this monetary pump priming and productivity and prices doing OK, money velocity has been in a notable downward trend. Therefore velocity seems to be an, if not the, anchor to growth.

Can the Fed control velocity? Well after trillions of dollars of stimulus later, one can plausibly argue no. While I agree with Friedman that inflation is always and everywhere a monetary phenomenon, there appears to be limited money turnover and demand, stunting the impact of increased monetary stimulus. That tells me that this is a fiscal policy, not a monetary policy, issue.

Therefore I am watching to see if there is a change in the fiscal environment as I feel that will move the needle macro economically long-term more than anything else. However this will require movement not from the Fed, which can only impact monetary policy—it will require movement from our federal and state legislatures and executives putting in place pro-growth fiscal policies.

Will it happen? One can only hope, and it bears watching closely as the New Year starts.