What most lay people don’t know about people in our industry is what complete number geeks we really are. Geeky to the point where we have passionate feelings about our preferred calculator brand. For instance, we named our graduate school intramural football team “The HP 12Cs”, after our financial calculator of choice. Yes, we are numbers driven people and are passionate on how they are used in the investment process depending on where we are in the investment cycle.

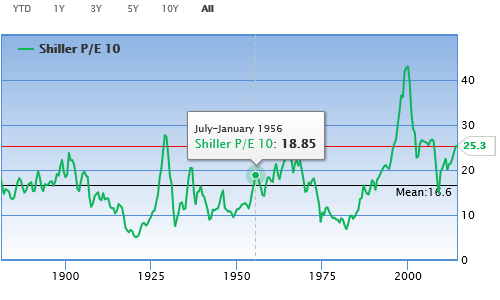

One thing I am noticing talking with fellow investors is how the numbers, as measured in earnings-based valuations, are leading them to fewer potential buy candidates as the market continues to grind higher. There have been non-stop debates if the market is under/overvalued since the beginning of this rally. As usual, it depends upon the numbers you look at for your reference point. The Schiller P/E chart, for instance appears to show that the market is near the top end of its historical range.

Chart: Historic Shiller P/E Ratios

(click on image to enlarge graph)

Source: gurufocus.com

Additionally, looking at corporate profits as a percent of GDP can lead investors to wonder where the next leg of earnings growth may be.

Chart: Corporate Profits After Tax/Gross Domestic Product

(click on image to enlarge graph)

Source: Federal Reserve Bank of St. Louis

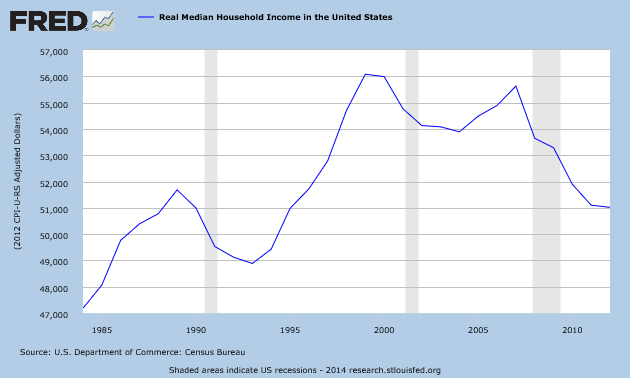

Sometimes, seemingly at least in part, at the expense of average household incomes.

Chart: Real Median Household Income in the United States

(click on image to enlarge graph)

Source: Federal Reserve Bank of St. Louis

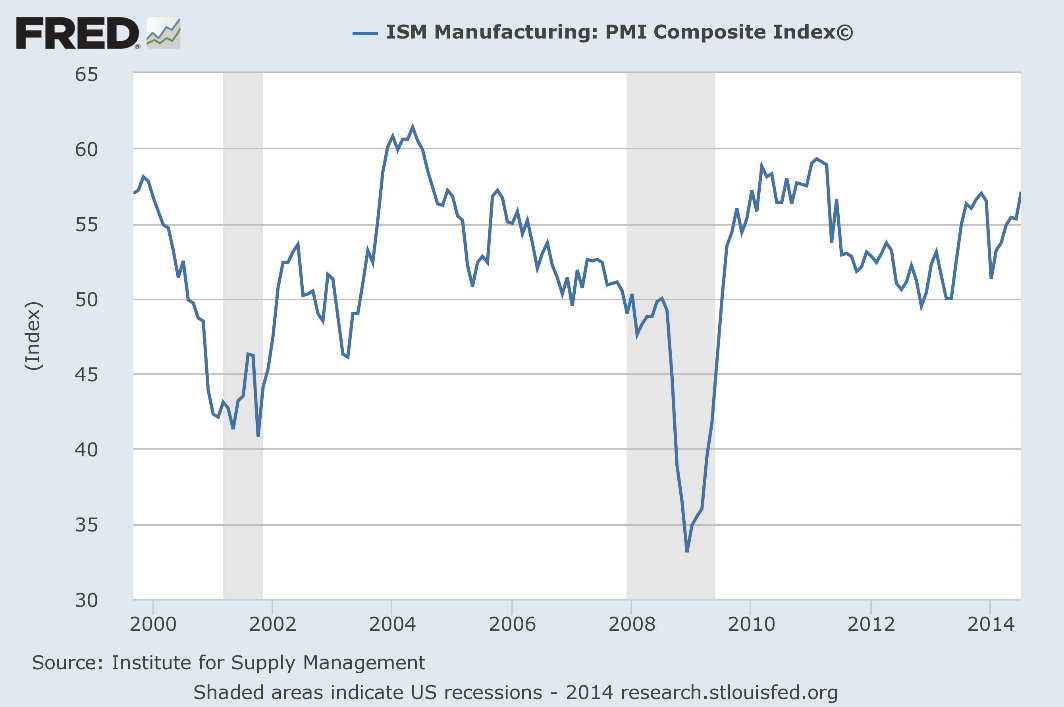

Still others offer compelling evidence (along with several charts, see link) that the market can continue to rally. Recent positive GDP data along with good ISM data (57.1, arguably a healthy reading and up from last month) and a progressing jobs picture may support further market gains.

Chart: ISM Manufacturing: PMI Composite Index

(click on image to enlarge graph)

Source: Federal Reserve Bank of St. Louis

Personal feelings on how the market will perform in the near/mid-term aside (I think we will do OK as long as the market has confidence in the Fed and its tactics and/or if it will come to the rescue every time the market has a hot lava burp), the question I normally ask myself when there is a lot of high valuation discussions is not what will the market do next, but what is the best valuation methodology to use with a given security at this stage of the cycle. Especially since so many of us need to be fully invested regardless of market conditions.

Why? Because usually when there is much debate about stock valuations being too high we investors sometimes can get caught up in earnings stories that will likely evolve beyond our investment horizon (if at all) to justify the current heightened valuation. This in my experience usually led me to two separate risks: getting led into a value trap hoping that a poorly run laggard would catch up to its peers over time or relying on earnings estimates two or even three fiscal years out.

Usually in these circumstances I tend to gravitate toward revenue based methodologies, such as price/sales and top line growth rates. I always thought that 50%+ of valuation work starts with revenues to begin with as so many estimates on all financial statements are driven by this line item. Additionally if the market continues to gravitate towards growth stocks I avoid value traps by only focusing on companies that can deliver on top line growth instead of focusing on margins and earnings that may never come. Conversely if the market begins to slip, if I focus on companies with a lower price to sales ratio, I don’t have to worry as much about discretionary actions a management team might do in a downturn such as delay or cut a stock buyback program, or what cuts they may make to “make the earnings number” in the short term but could harm future growth.