Back in 1972 after Nixon’s landslide re-election Pauline Kael, the film critic at the time for the New Yorker magazine allegedly quipped “I can’t believe Nixon won. I don’t know anyone who voted for him.” While it’s a matter of debate if she actually said this, the point is still clear—sometimes we let our own circumstances and biases cloud our interpretation of data.

For instance we were listening to one market prognosticator that said that he thought that we might be seeing a new level of frugality among consumers that we have not seen in several decades, which might explain some of the recent data and resulting market action. While we believe that the consumer is more cautious than in time’s past, we also think that the data has reflected consumer caution for a while. Why the discrepancy? In our observation since us investment types make our living in part off the performance of the market, sometimes we confuse a rising market with rising fortunes for Americans in general. Therefore it can be easy therefore to neglect data that contradicts our own personal experiences even though it might not reflect what the rest of the country is experiencing.

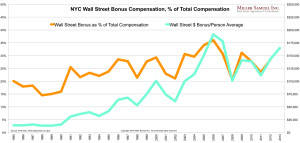

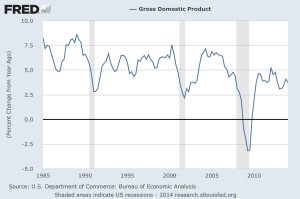

One such brief example may be comparing the New York Wall Street bonus average per employee to that of various income level increases in the United States. While the bonus of the average Wall Streeter has remained relatively strong as of late, the real median household income has not been as robust. While admittedly the latter is inflation adjusted, one gets the general idea. Plus we haven’t seen much of inflation the last several years. Plus GDP data has been arguably mundane the past few years.

NYC Wall Street Bonus Compensation, % of Total Compensation

Real Median Household Income in the United States

Gross Domestic Product

Therefore sometimes we investors might have to be cautious in interpreting a strong market with a strong consumer or a strong economy.